Reblogged from Brintab

In February, 2026 Team Trump’s Iran threats turned into an attack, accompanied by Israeli forces. While not losing sight of the painful human impact of war, I will focus here on what affects your investments. War usually has specific and general investment implications. The specific implications relate to the industries and jurisdictions directly impacted, and the general relate to indirect effects and the economy overall. With respect to the specific, obviously the oil industry was the most directly impacted but also fertilizers, airlines, aluminum smelting, and shipping, to name a few. Those businesses operate directly in the affected region.

With respect to the more general, all downstream industries are affected. Airlines are not only affected by being unable to fly through the Middle East but also by the escalating cost and even unavailability of fuel as well as slack demand caused by the higher prices and by traveller unease. All buyers of oil and gas for fuel or for petrochemical feedstock are impacted. Farm users of fertilizers are affected. Aluminum users (due to curtailed Middle East aluminum smelting) are affected. All these direct factors ripple through to impact the pricing of end products. This price impact is compounded by the need for increased government spending (war is expensive) and the two lead to inflation.

We don’t know if the impact will be a short-term blip or if it will drag on. That is what the investment world is trying to figure out. There have been recent remarks by President Trump, Prime Minister Netanyahu, and Iranian leadership indicating an interest in de-escalating but of course each of them wants that to happen purely on their own terms, which is clearly unrealistic. In time we will see if there is convergence of the positions of the three parties. While Iran is weaker militarily, the country’s strong position relates to its ability to keep international oil prices escalated for a duration that causes severe economic pain to the others. Hence the game of chicken where the attackers mainly hold military weapons and the defender mainly holds economic weapons. I do believe that the war will settle down by late this year but even so, the negative supply chain consequences will take much longer to remedy.

Bonds and Interest Rates

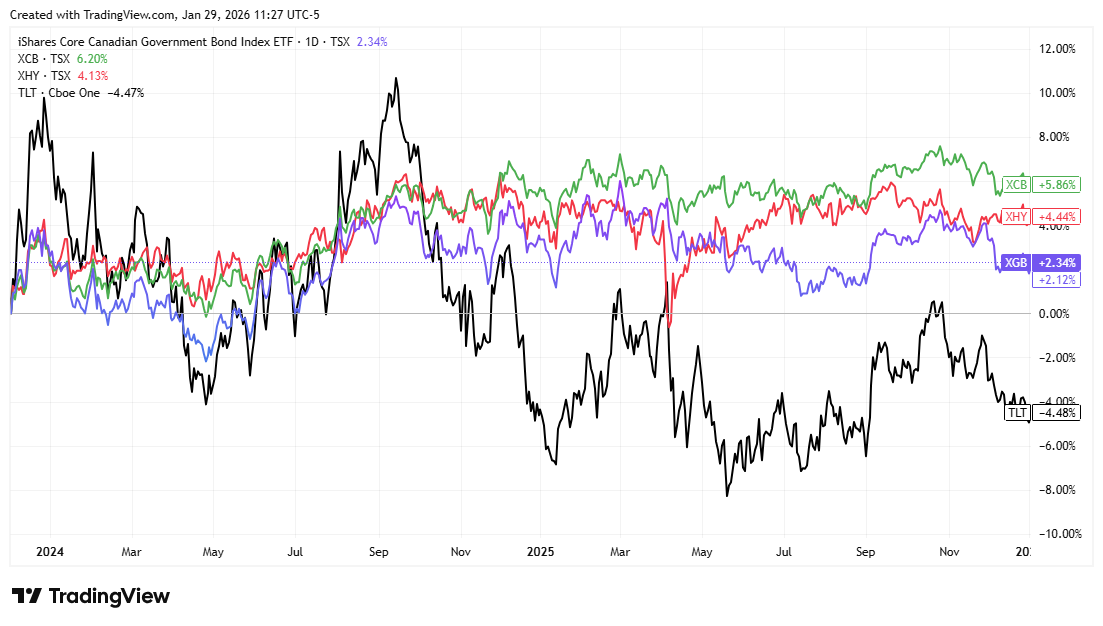

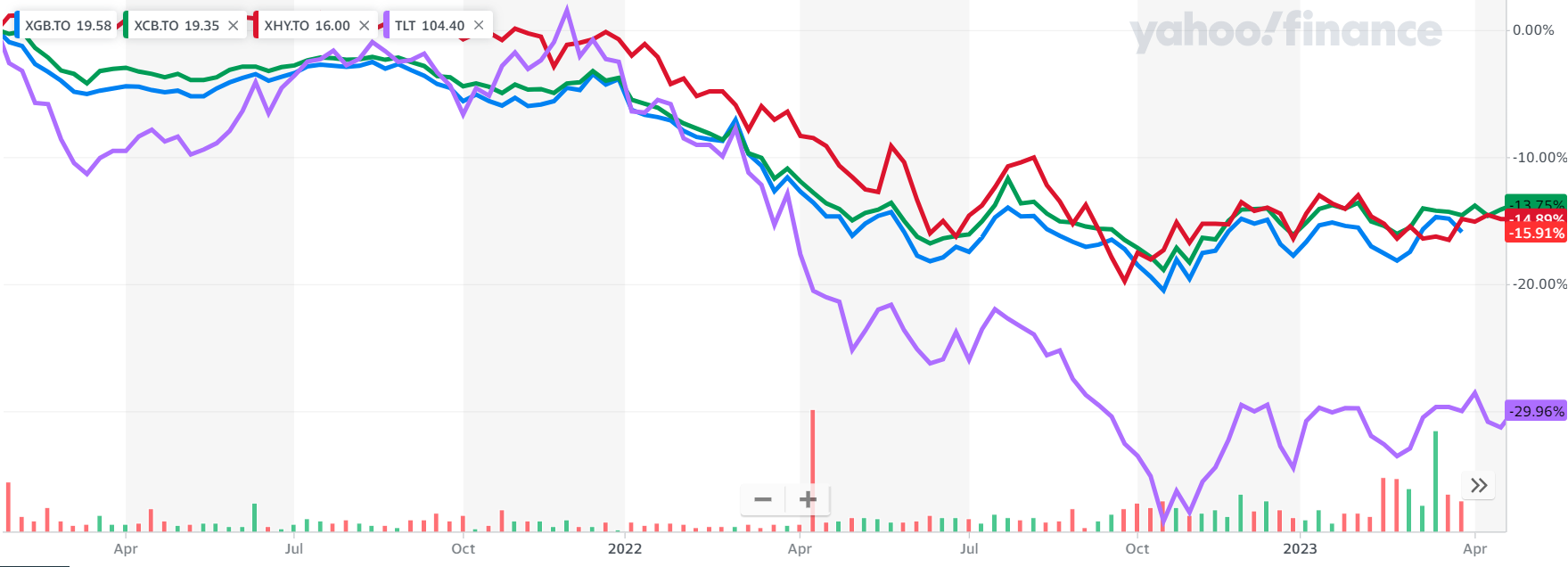

Inflation is one of the main drivers of interest rates and the outlook had been downward prior to the inflationary trigger of high oil prices and likely high level of spending by the US government. This has led us to a rethink of the direction of interest rates and is creating an increased risk of stagflation, where the labour market and the economy are floundering while inflation is still running higher than desired!

Due to our prior expectations for declining inflation, our expectations for short-term and long-term interest rates were trending downward early in 2026. Our expectations reversed course and moved upwards through March. I expect the “hot war” will be over in a few months and near the end of the year people will stop projecting sky-high oil prices. Nonetheless, because so much equipment has been damaged around the Middle East it will take some time for various businesses to be able to resume full operations and supply chains to recover. In the meantime, that inflationary strain will still be felt.

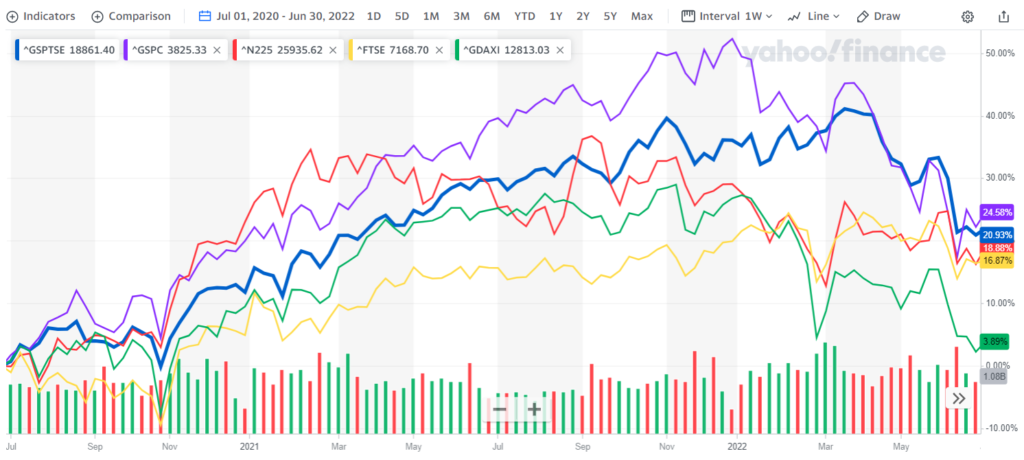

Fig. 1: Bonds-Med. term Cdn Gov’t-purple, Cdn Corp-green, High Yield-red, Long Term US-black – 2 years – TradingView

At the same time, we are seeing weaker signals in the economy overall. Recent reports on the US labour market show an increased number of part time roles and much of the job growth being driven by government and healthcare. The consumer side of the economy is clearly struggling. At the 2025 year end we had dialed back our recession probability to 50:50 but with the skyrocketing cost of oil we see the likelihood of a recession rising once again. It is not typical that we need to flip-flop like this but then again, the actions of late February are not typical either. When the facts change, we change our perspective.

The weakening labour market alongside rising inflation creates the central banker’s dilemma we call stagflation. Should they drop interest rates to coax the economy or jack up interest rates to slow down price increases? There is no easy answer. Past oil price cycles lead me to believe that there is a good chance the price escalation leads to a recession.

For bonds, this means that even if the 10-year bond interest rate trajectory is higher for the next little while, by a year from now we anticipate it declining again. There is one caveat to this. As the US debt load starts to worry more and more investors, the yield they demand for holding US bonds may rise. Remember that higher bond yields imply lower bond prices so our general preference is declining yields that push bond prices up.

Currencies

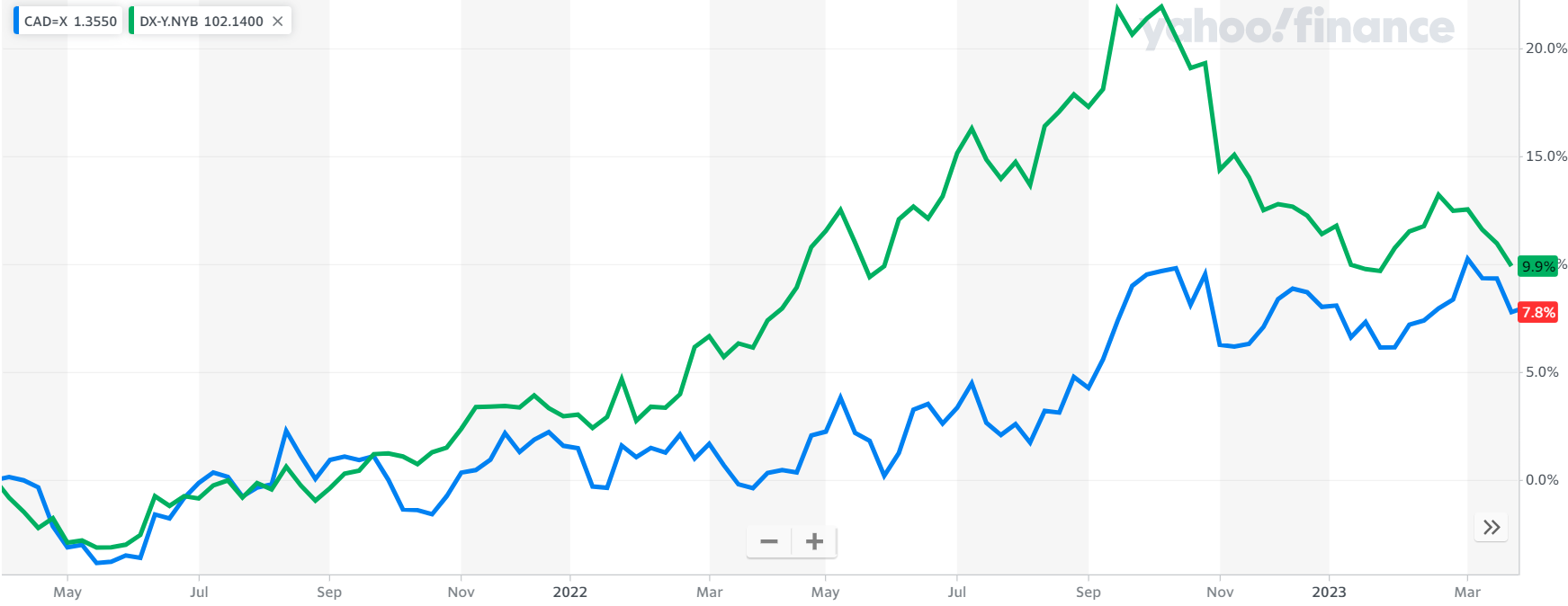

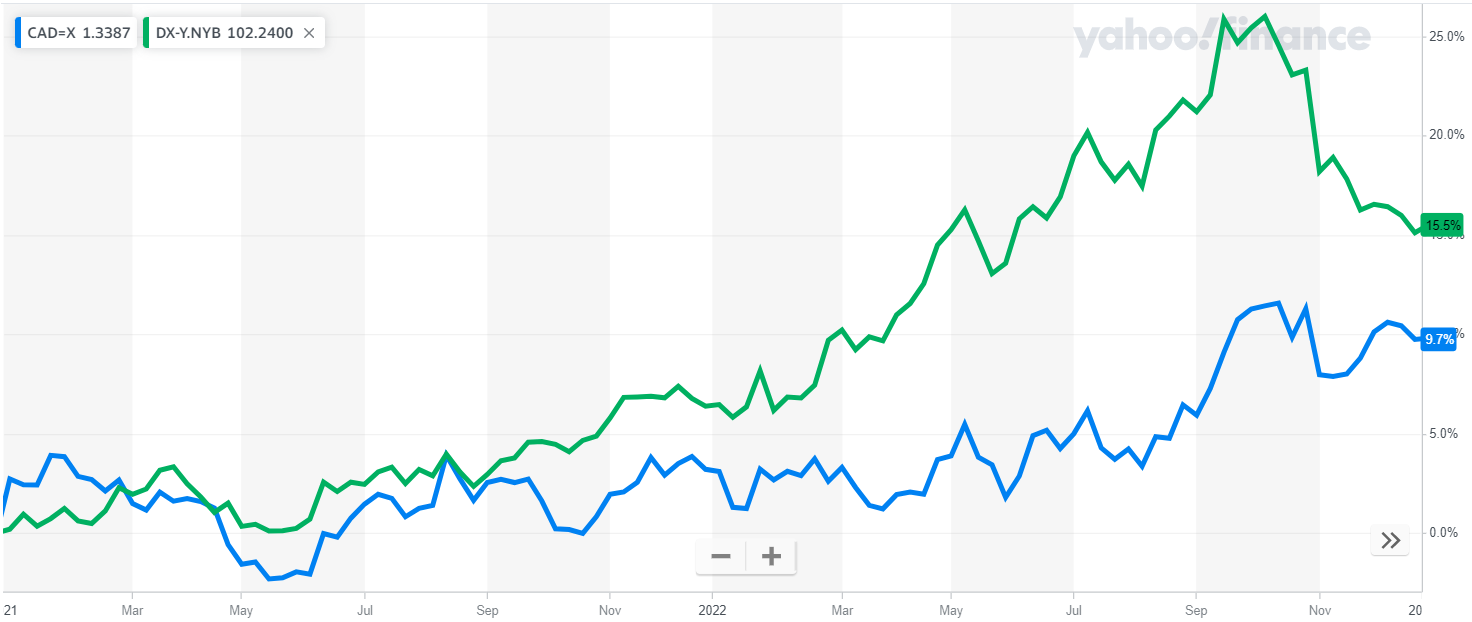

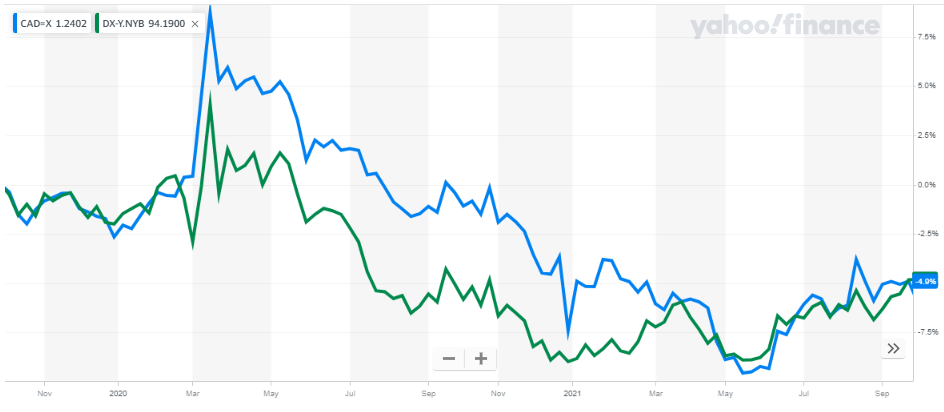

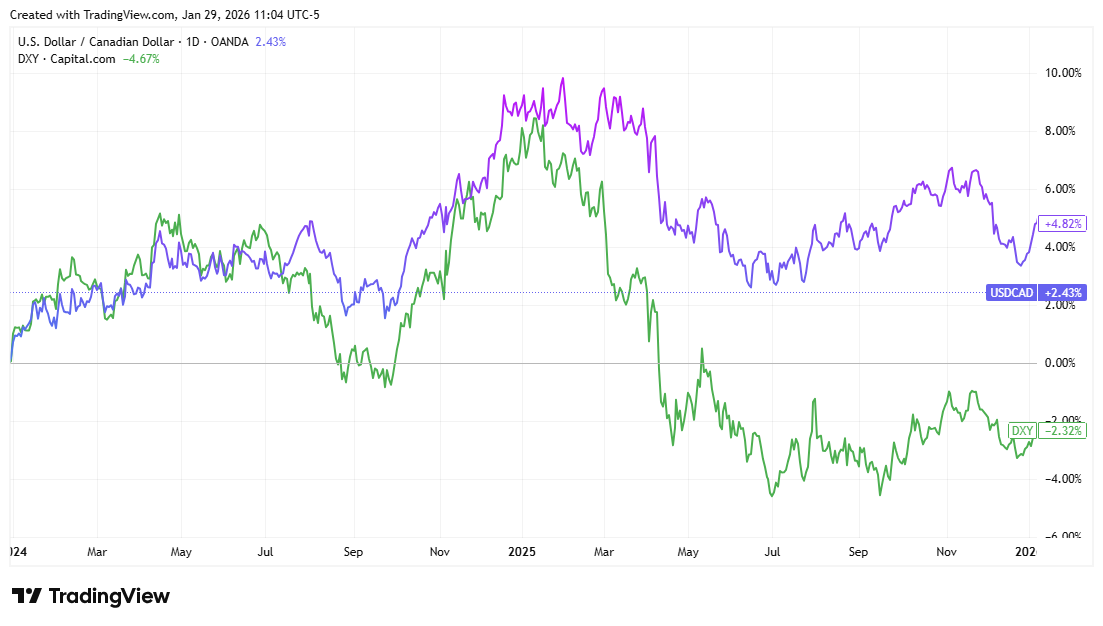

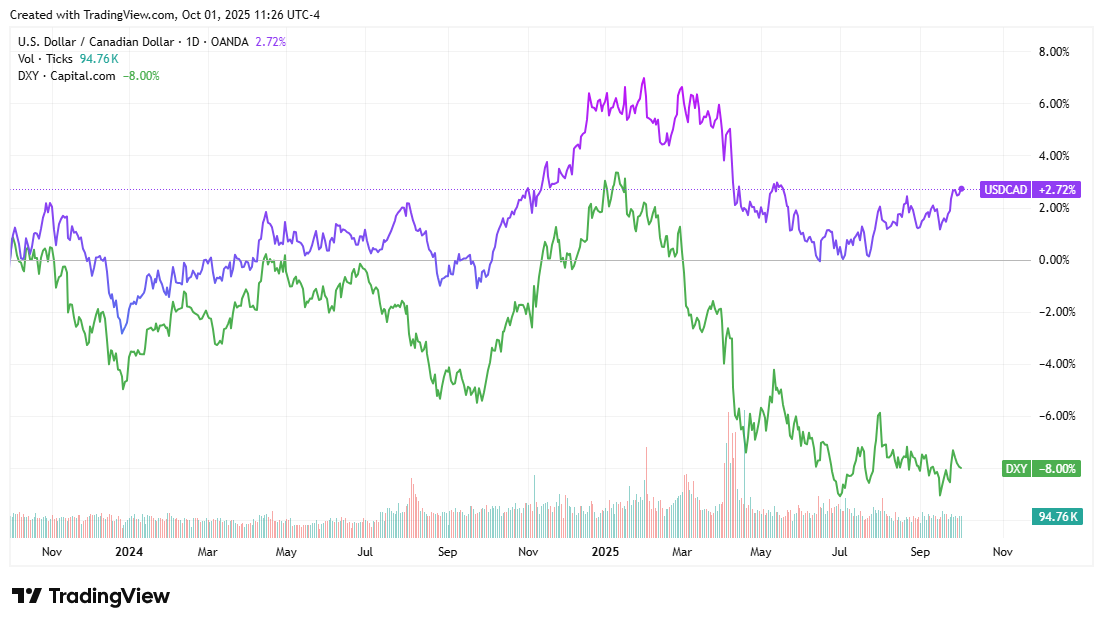

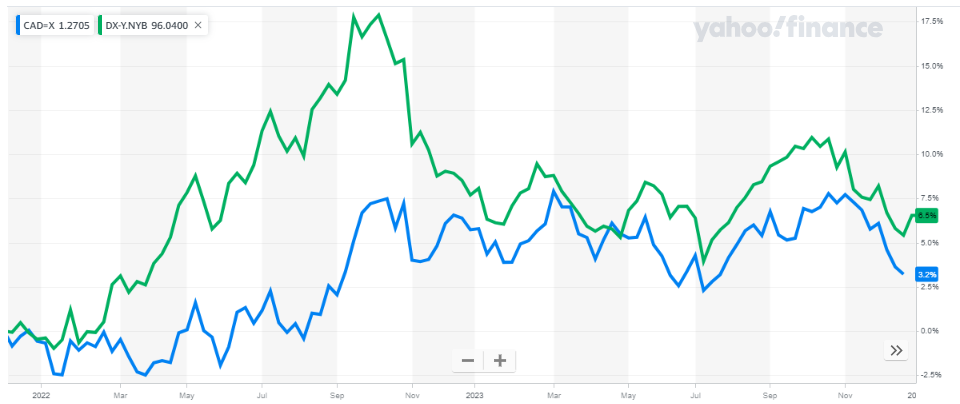

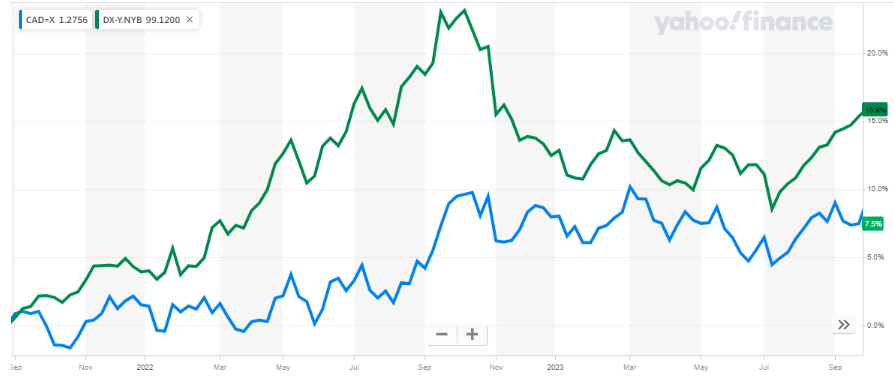

In early 2026 the USD weakened against the CAD and other currencies as the recession risk faded but once the Iran attack happened, we see that through the month of March, 2026 the USD strengthened again. The flight of capital to safe haven currencies like the USD returned. Note that after the end of March (not shown here) the USD weakened again as investors hoped for a relatively quick resolution to the Middle East hostilities. There is a good chance that will be short-lived and there will be yet another resurgence of the USD. The driver this time will be the return of recession risk and the increased volatility in emerging market investments in anticipation of such an occurrence.

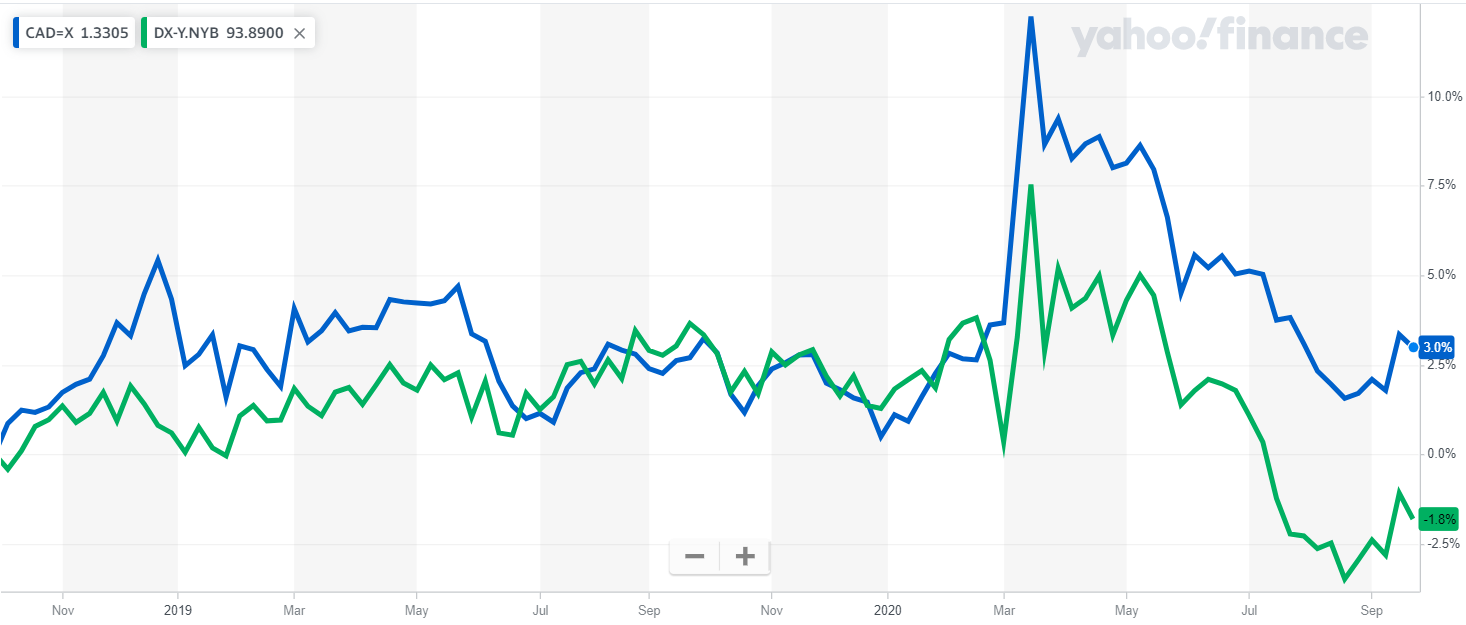

Fig. 2: US Dollar Index-green and USD vs CAD-purple – 2 years – TradingView

Also, as it specifically relates to the CAD/USD exchange rate, there is still the overhang of the CUSMA negotiations ahead of us. There is a good chance this will push the CAD lower through the middle of this year however we have already seen the Carney government telegraphing to the public that these CUSMA negotiations will be difficult and we should expect some pain. I believe they are steering markets to gradually pull back and absorb the risk (which shows up in lower prices) now so that there will not be an extreme economic shock come summer.

Stock Markets

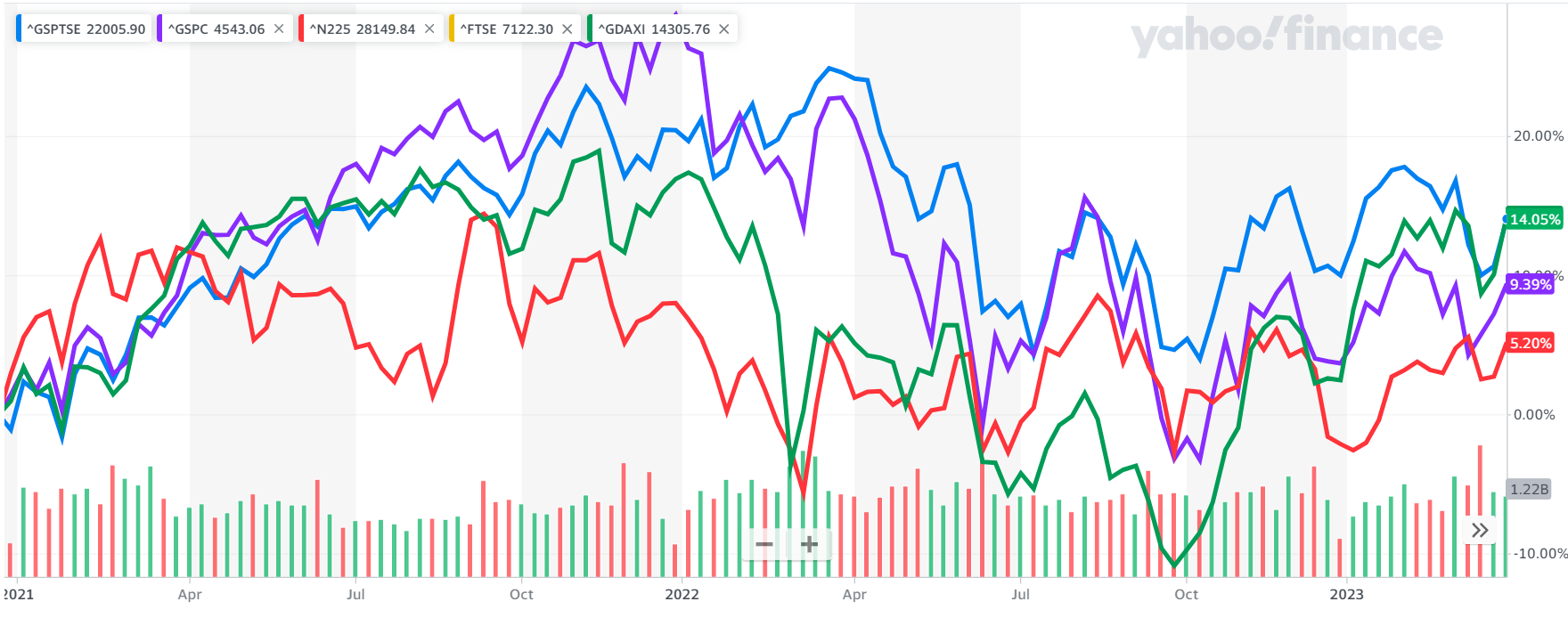

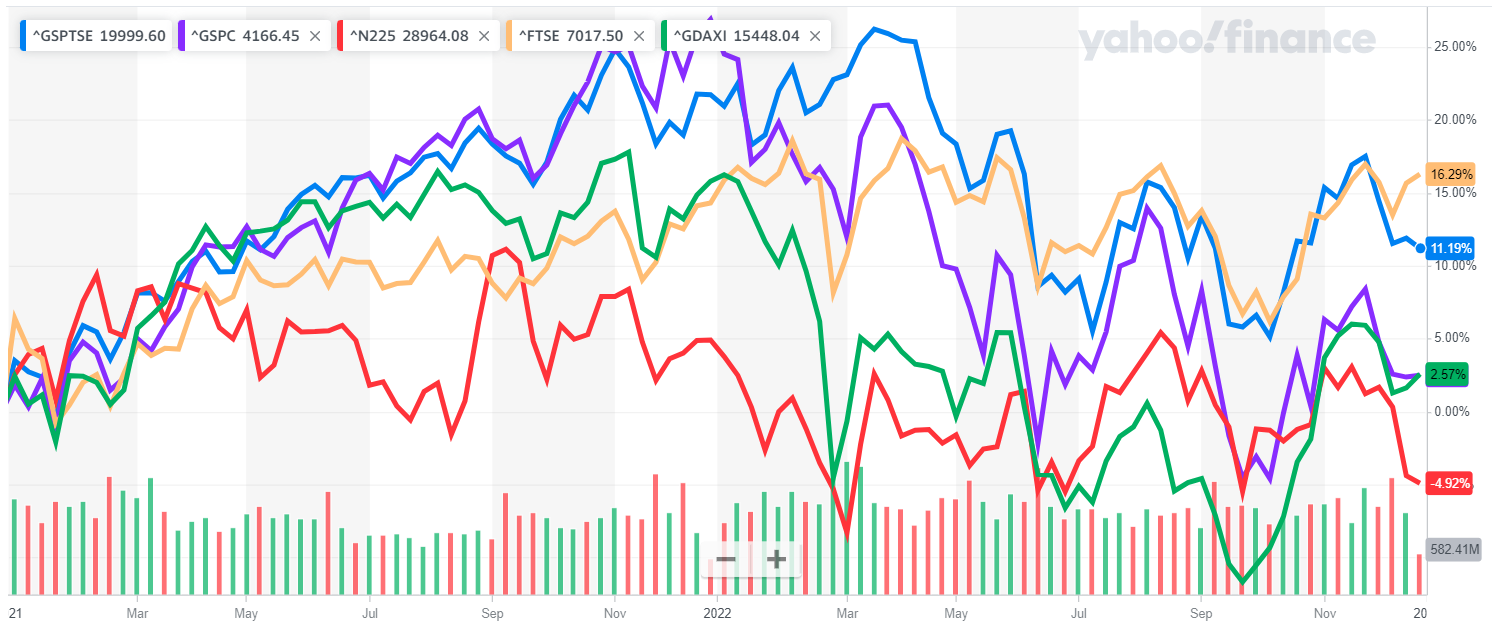

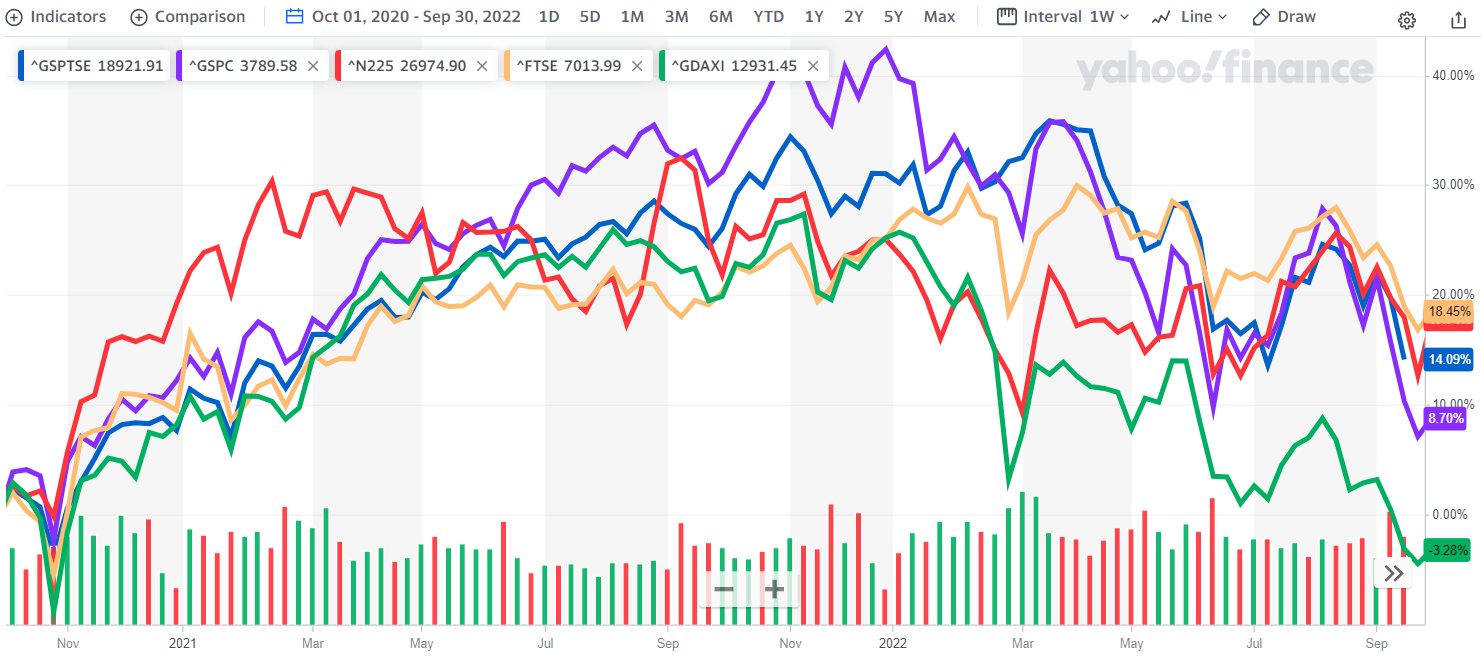

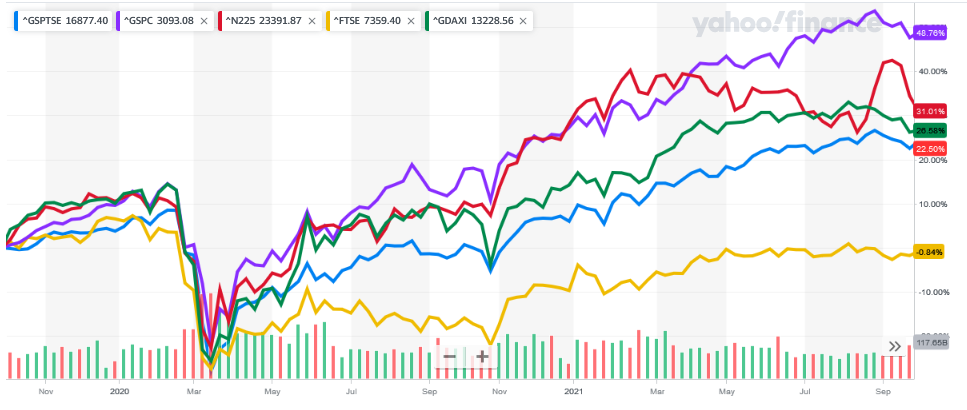

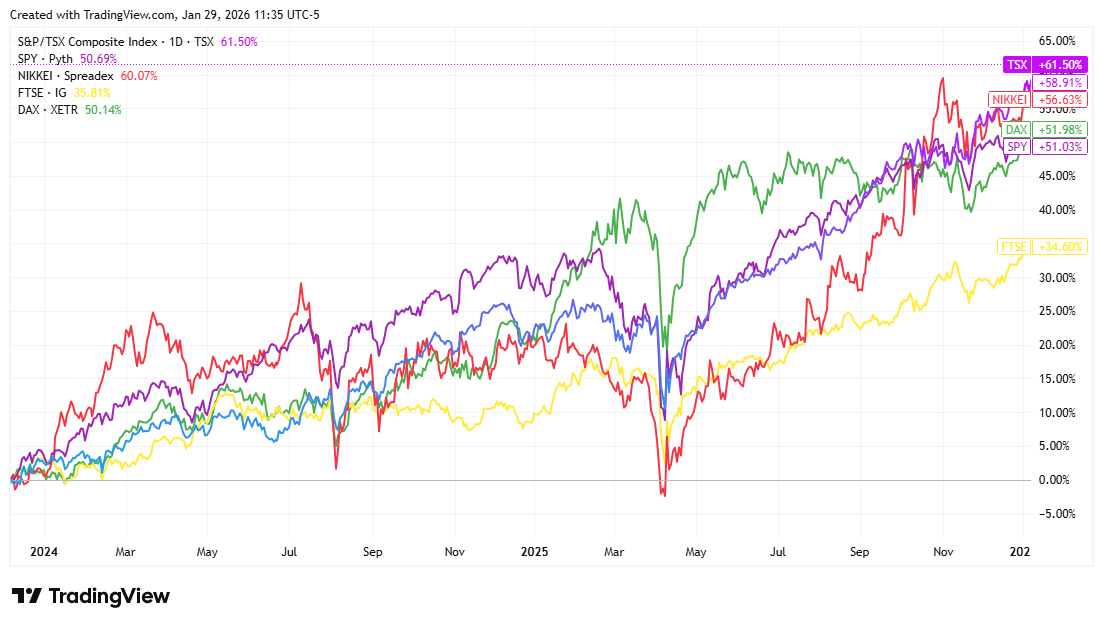

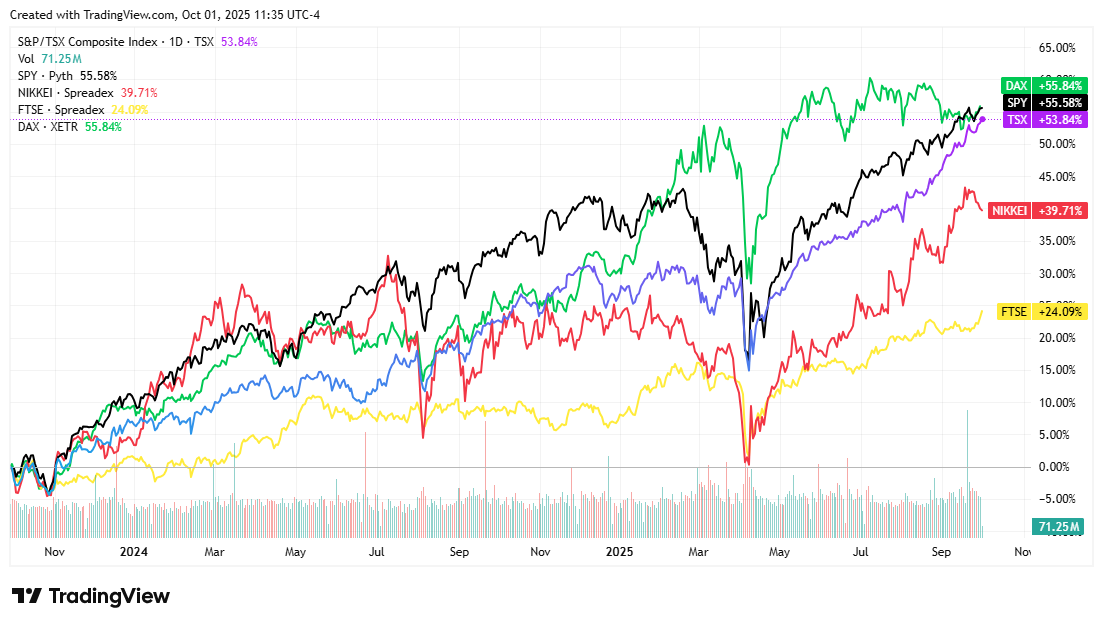

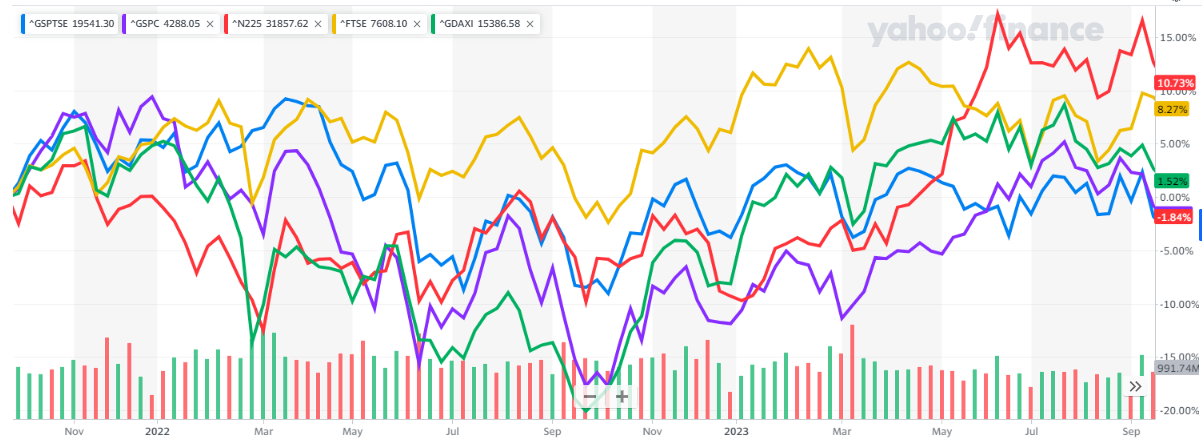

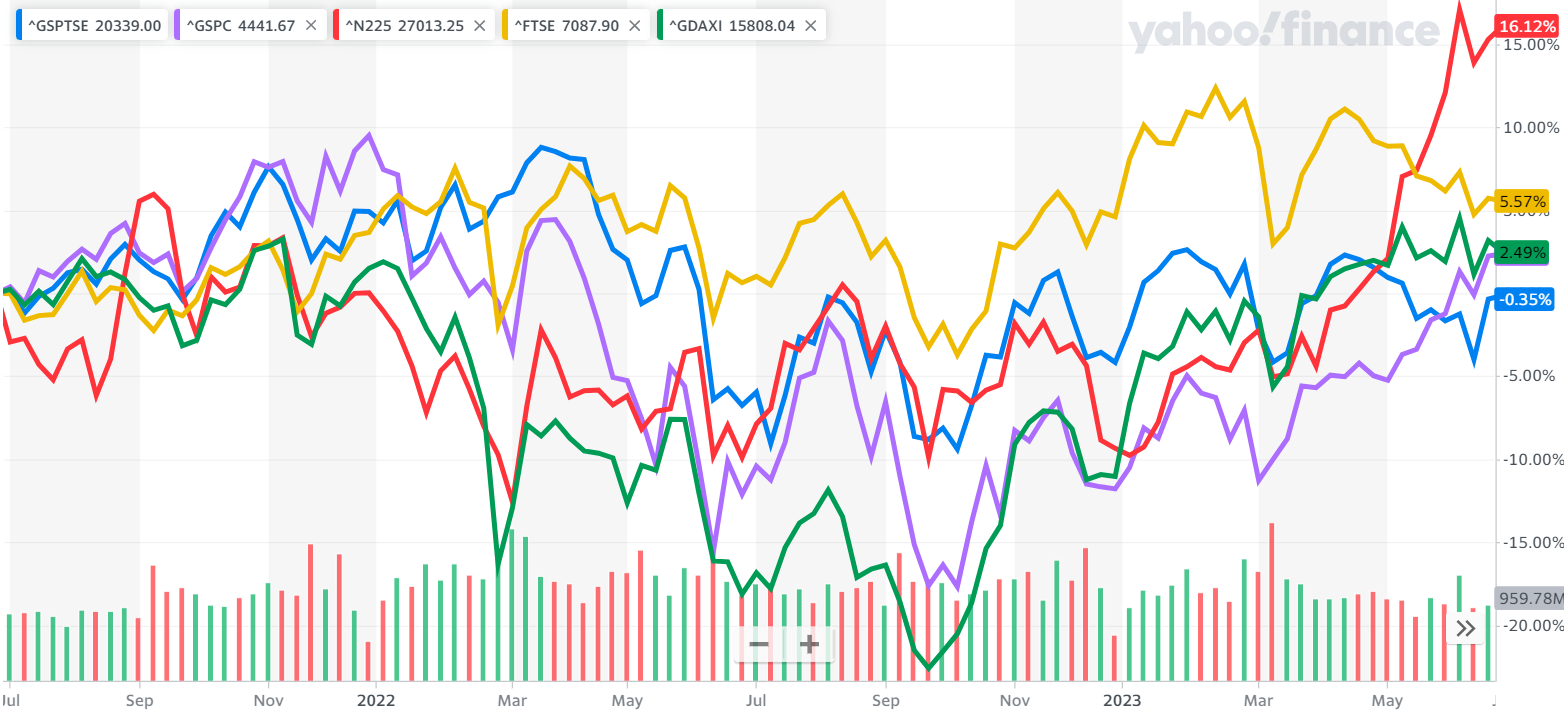

Equity markets had been pretty flat overall in January but the average was masking what was happening at the sector level. Defensive sectors like consumer staples and utilities were doing well while other sectors like financials and technology were declining. Then in March, following the attack on Iran all major sectors except energy sold off. We executed on a couple buying opportunities when stocks were cheap, acting against the panicky market. Although we saw this as a buying opportunity, that is not to say we always go against the market. To automatically take contrarian actions blindly would be naïve, but we do look for moments when we think the rush of the crowd is giving us a gift.

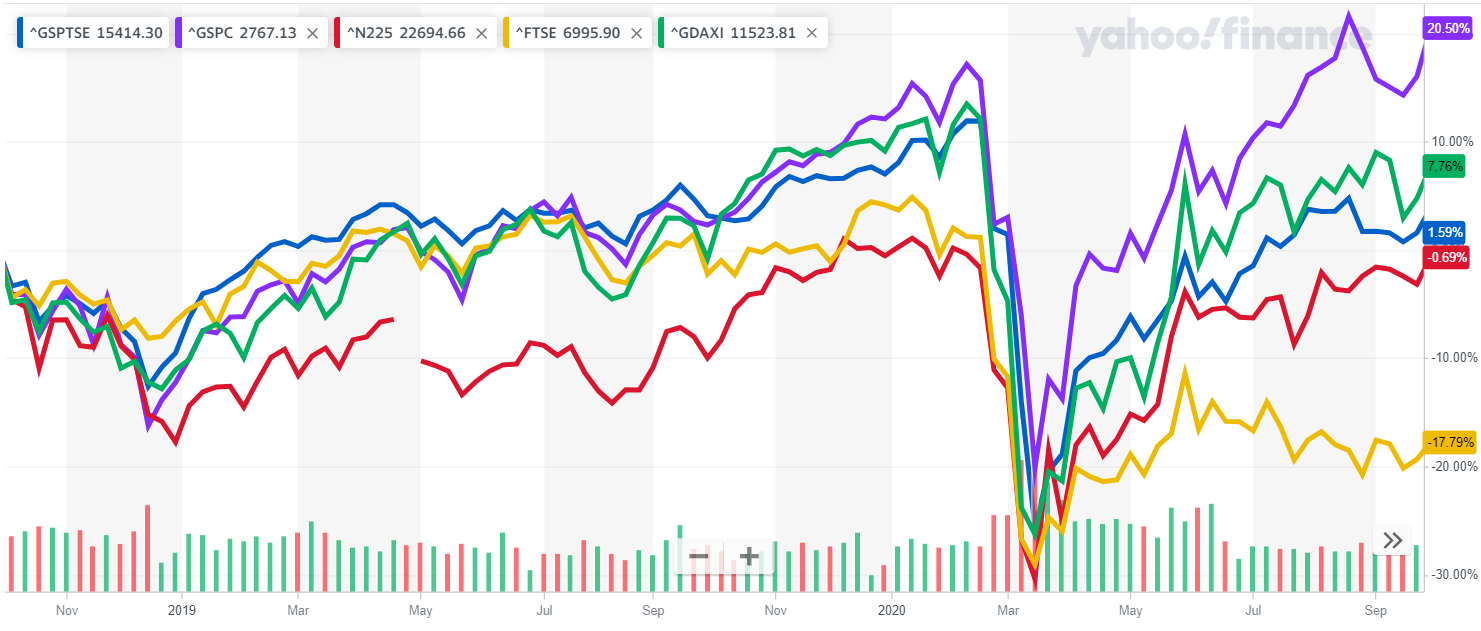

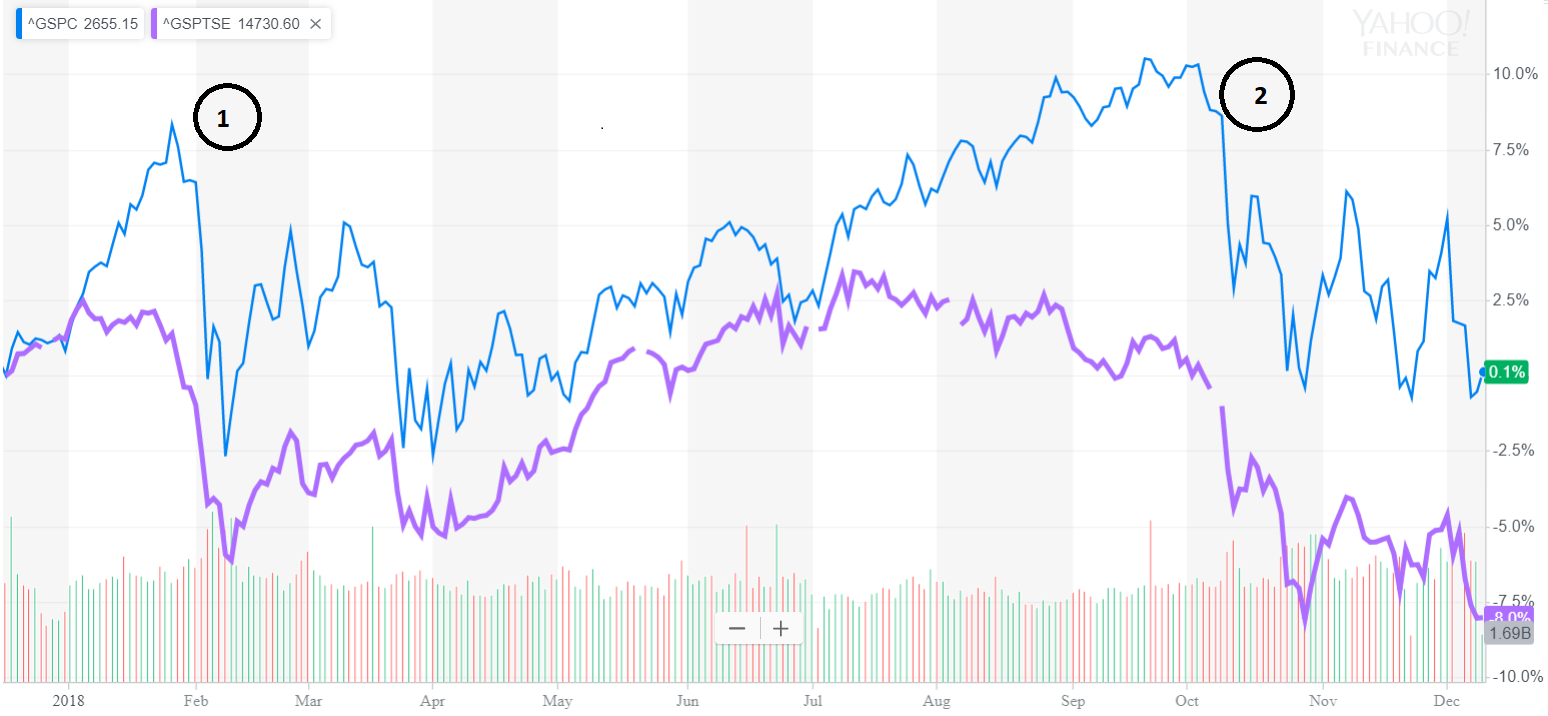

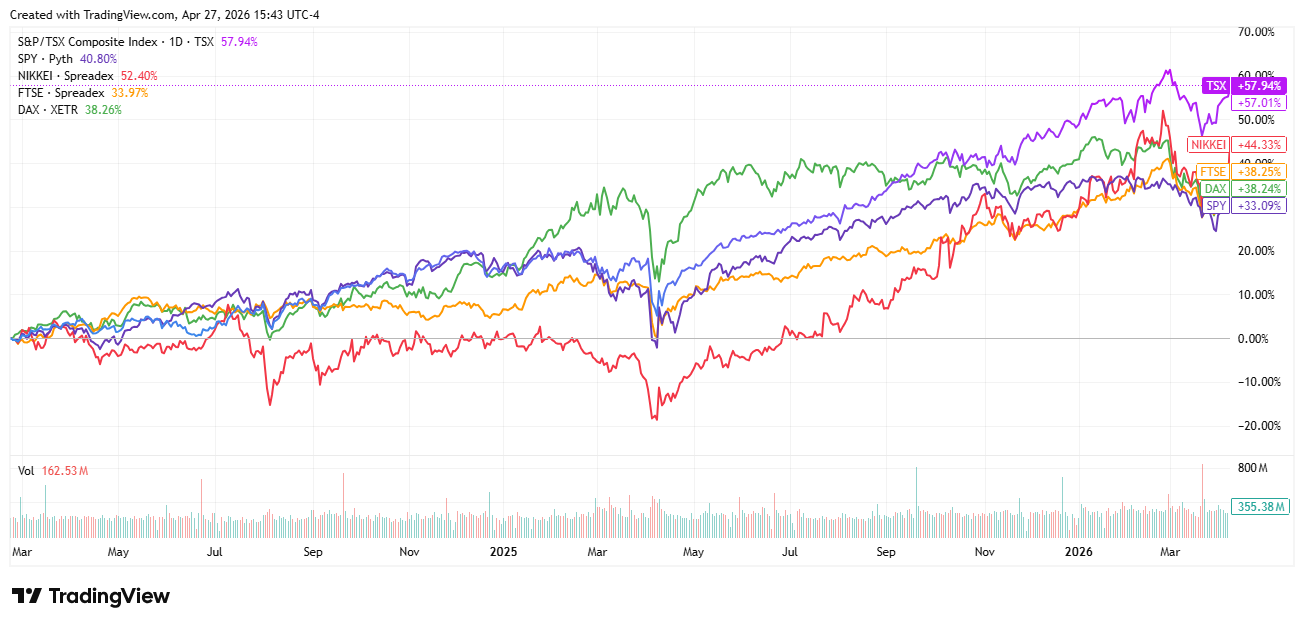

Fig. 3: Stocks: US-black, Can-purple, Jpn-red, UK-yellow, Germany-green – 2 yrs – Trading View

Although the market has recovered from plummeting in March, we still see opportunities in a variety of businesses and are currently sifting through them to establish our priorities with respect to which have the strongest long run prospects.

Respectfully submitted,

Paul Fettes, CFA, CFP, Chief Executive Officer, Brintab Corp.

Fig. 1: Bonds-Med. term Cdn-blue, Corp-green, High Yield-orange, Long Term US-purple – 2 years – Yahoo Finance

Fig. 1: Bonds-Med. term Cdn-blue, Corp-green, High Yield-orange, Long Term US-purple – 2 years – Yahoo Finance Fig. 2: US Dollar Index (green) and USD vs CAD (blue) – 2 years – Yahoo Finance

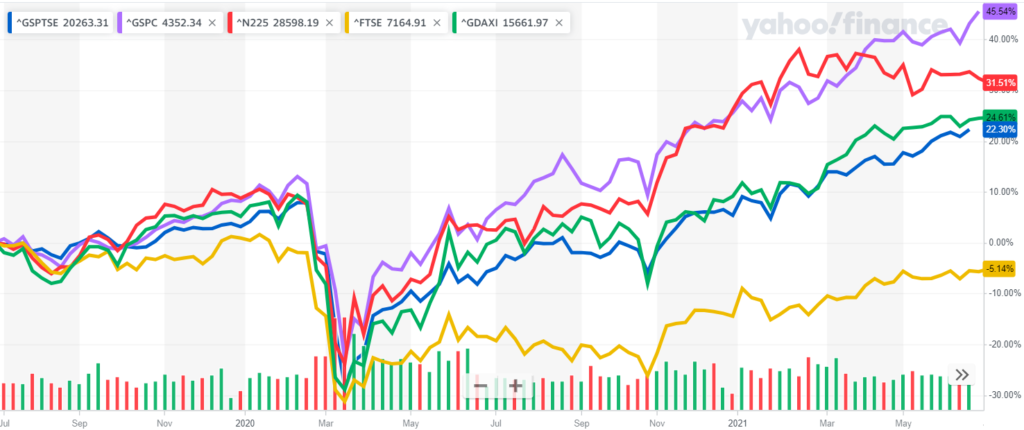

Fig. 2: US Dollar Index (green) and USD vs CAD (blue) – 2 years – Yahoo Finance Fig. 3: Equities: US-purple, Can-blue, Jpn-red, UK-yellow, Germany-green – 2 yrs – Yahoo Finance

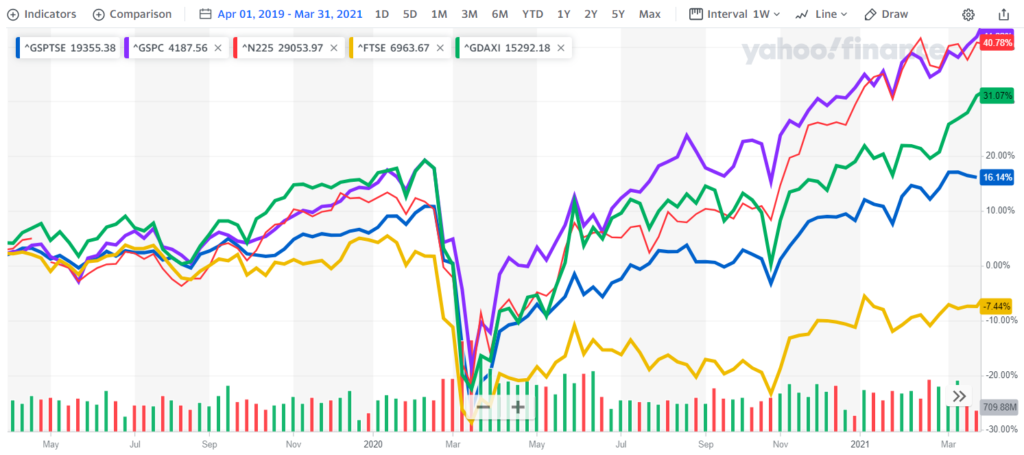

Fig. 3: Equities: US-purple, Can-blue, Jpn-red, UK-yellow, Germany-green – 2 yrs – Yahoo Finance Fig. 1: Bonds-Med. term Cdn-blue, Corp-green, High Yield-orange, Long Term US-purple – 2 years – Yahoo Finance

Fig. 1: Bonds-Med. term Cdn-blue, Corp-green, High Yield-orange, Long Term US-purple – 2 years – Yahoo Finance Fig. 2: US Dollar Index (green) and USD vs CAD (blue) – 2 years – Yahoo Finance

Fig. 2: US Dollar Index (green) and USD vs CAD (blue) – 2 years – Yahoo Finance Fig. 3: Equities: US-purple, Can-blue, Jpn-red, UK-yellow, Germany-green – 2 yrs – Yahoo Finance

Fig. 3: Equities: US-purple, Can-blue, Jpn-red, UK-yellow, Germany-green – 2 yrs – Yahoo Finance

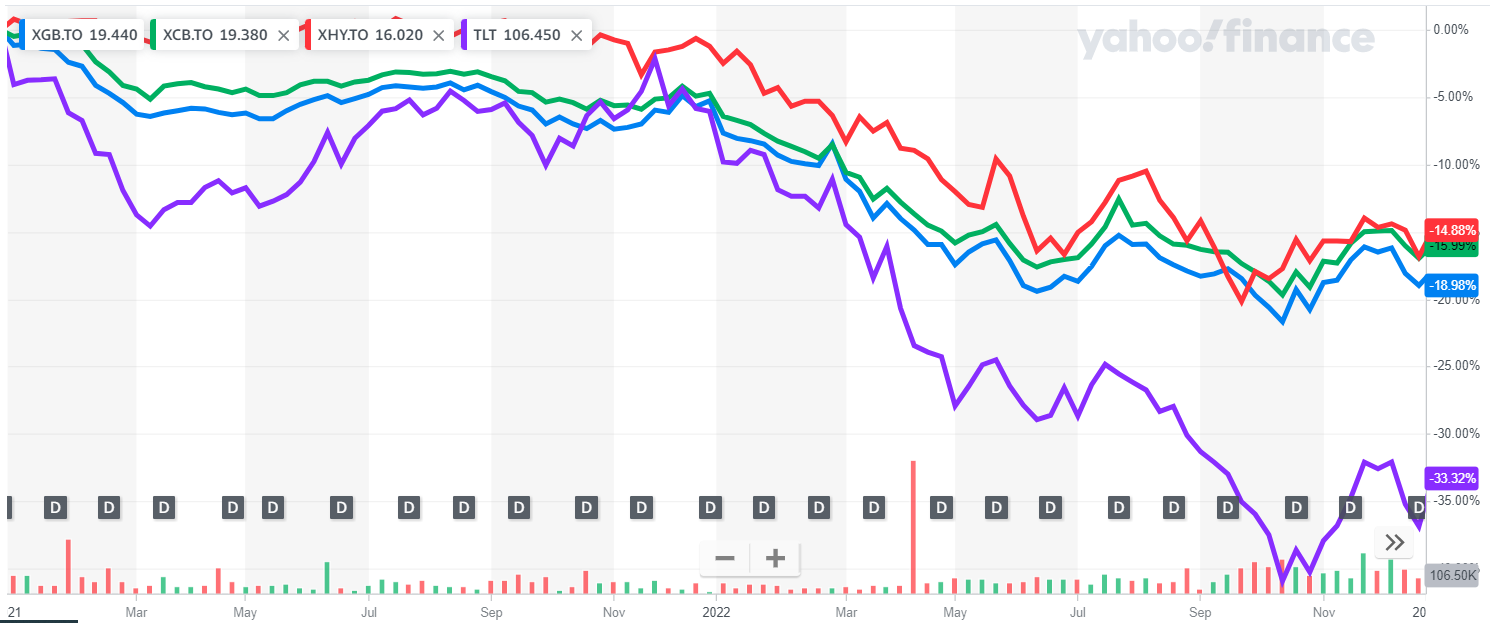

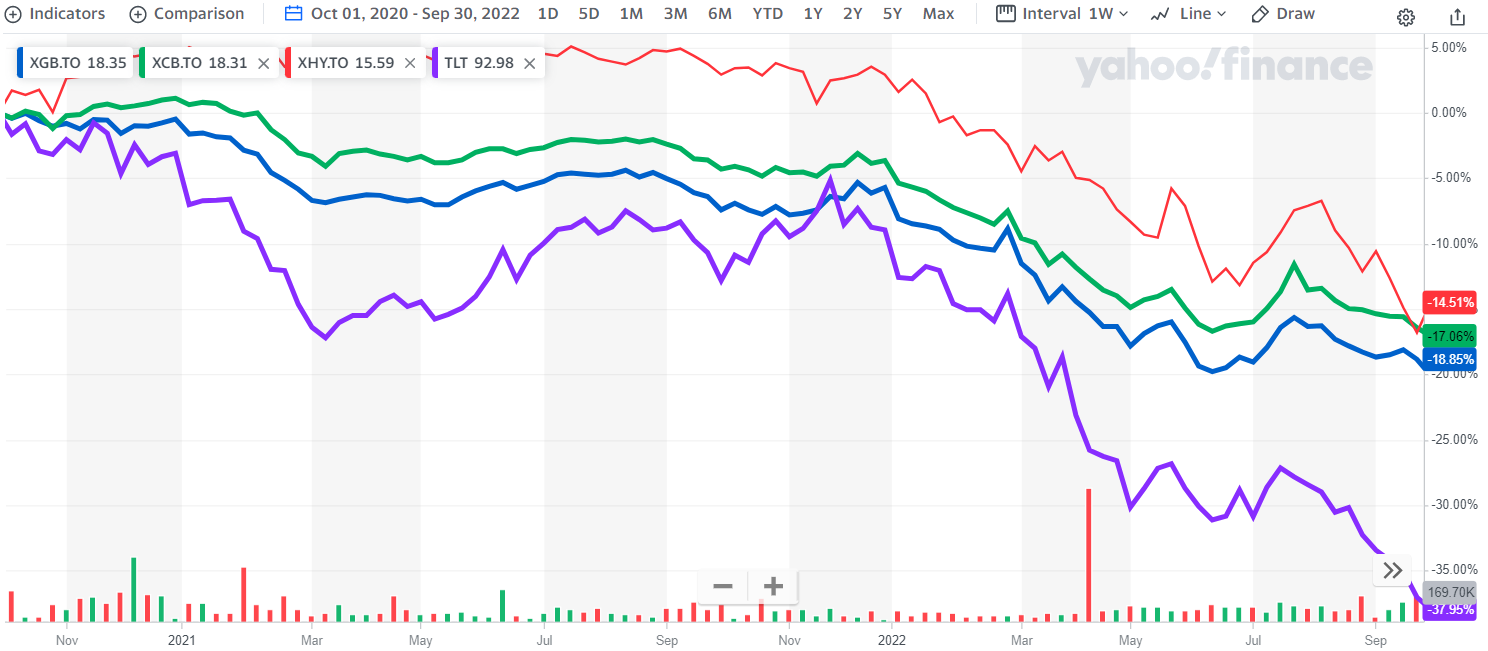

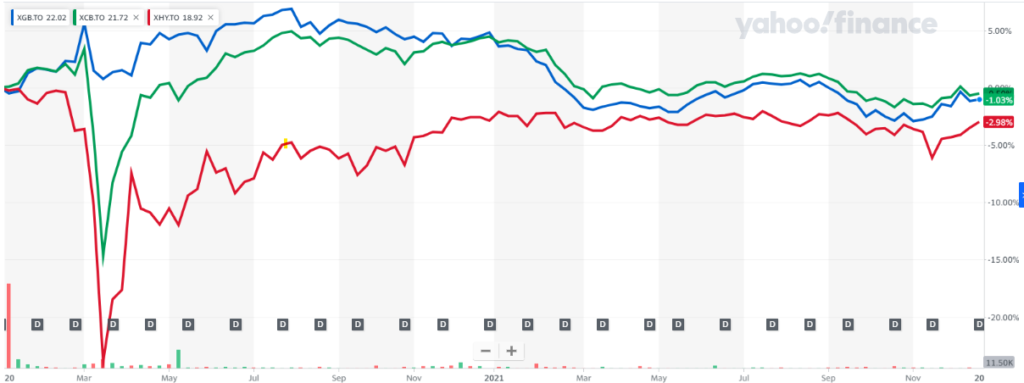

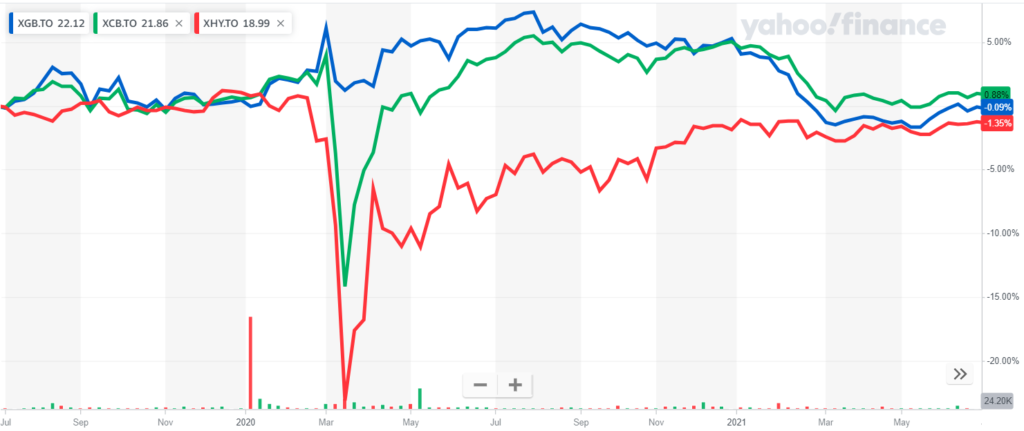

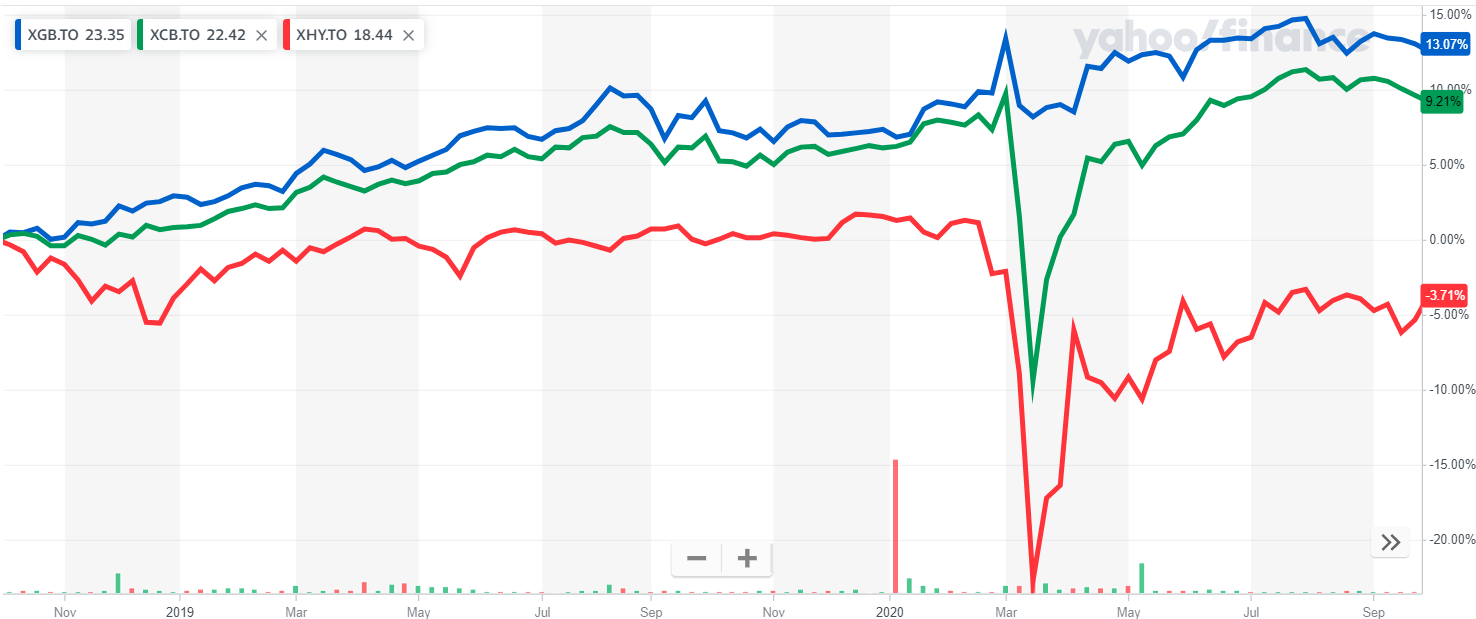

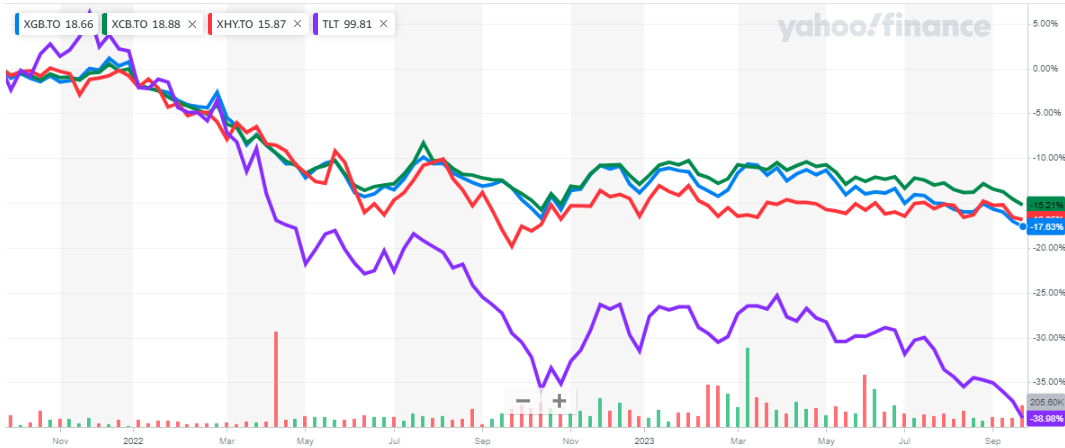

Fig. 1: Bond ETFs: Gov’t:XGB, Corp:XCB, High Yield:XHY, US 20-yr:TLT–2 yr –Yahoo Finance

Fig. 1: Bond ETFs: Gov’t:XGB, Corp:XCB, High Yield:XHY, US 20-yr:TLT–2 yr –Yahoo Finance Fig. 2: US Dollar Index (green) and USD vs CAD (blue) – 2 years – Yahoo Finance

Fig. 2: US Dollar Index (green) and USD vs CAD (blue) – 2 years – Yahoo Finance Fig. 3: Equities: US-purple, Can-blue, Jpn-red, UK-yellow, Germany-green – 2 yrs – Yahoo Finance

Fig. 3: Equities: US-purple, Can-blue, Jpn-red, UK-yellow, Germany-green – 2 yrs – Yahoo Finance

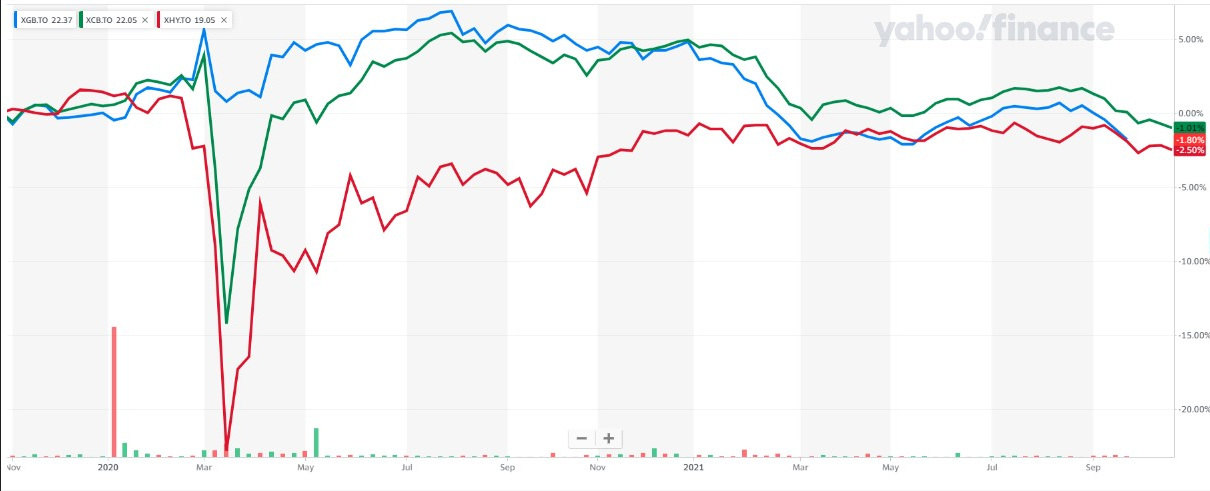

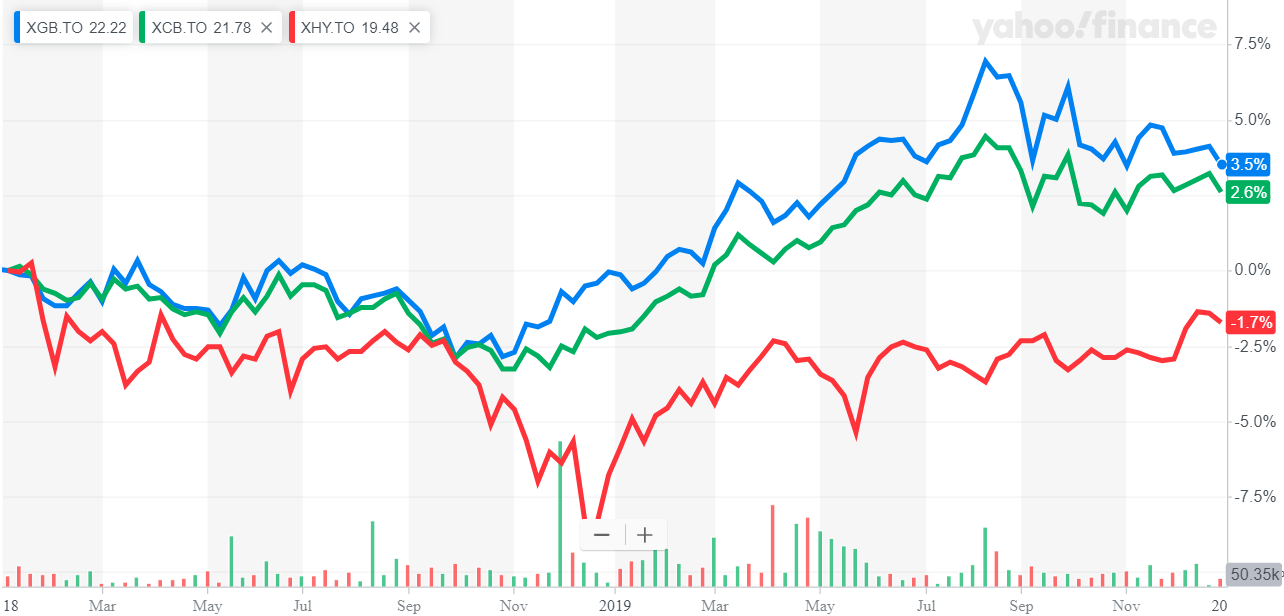

Fig. 1: Bond ETFs: Gov’t:XGB, Corp:XCB, High Yield:XHY, US 20-yr:TLT–2 yr –Yahoo Finance

Fig. 1: Bond ETFs: Gov’t:XGB, Corp:XCB, High Yield:XHY, US 20-yr:TLT–2 yr –Yahoo Finance